10 min read

Why Debt Consolidation Is About Psychology, Not Just Numbers

-

-

Copied link to Clipboard!

Copied link to Clipboard!

Have you ever looked at your budget and wondered how you will cover all your bills? If you’re feeling constantly behind as you navigate your debt, there is a reason. Debt is math, but it also requires attention and introduces stress and mandatory routines. Each extra account adds another due date and another minimum payment. Even worse, it leaves you feeling like you are one mistake away from chaos.

In debt consolidation psychology, the numbers matter, but so does the structure of your debt system. When the plan is easier to run, you follow through more often. That follow-through is what pays off debt.

Lesson Notes:

Lesson Notes:

- Debt stress comes from complexity, decision fatigue, and constant mental tracking.

- Consolidation helps by creating one clear payment, reducing cognitive load.

- The best payoff plan is the one you can sustain consistently.

- Consolidation success needs stable income, better terms, automation, and stopping new debt.

LESSON CONTENTS

Why debt feels overwhelming even when the math works

A lot of people assume that if the math works, the stress should disappear. In reality, when you manage debt, you are dealing with its complexity not just your balances. Managing multiple accounts can create decision fatigue. You keep choosing what to pay, when to pay, and how much to pay. Over time, these small choices drain mental energy and make it easier to procrastinate. You might be doing everything right and still feel overwhelmed.

Research supports this. In one study on debt and cognition, the authors wrote: "Taken together, debt mental-accounting costs appear to cause greater impairment of psychological and cognitive functioning than debt levels do." (Ong et al., 2019). In plain terms, tracking debt taxes your brain even before the interest rate does.

When your mind is overloaded, it’s harder to keep up with the habits that keep you on track. You might miss a payment because you forgot a due date or avoid opening statements because they make you anxious. Stress can also lead to impulsive choices, making you focus only on what feels urgent or comforting right now. This is how debt quietly gets in the way of your budgeting and good intentions.

The emotional cost of carrying multiple debts

When debt keeps stressing you out, it makes you feel less secure each month. Instead of planning ahead, you’re just trying to get by. You end up dealing with late fees, overdrafts, surprise bills, and the fear that one tough week could set you back. That’s why debt can feel personal, even if it started with something practical like car repairs or a medical bill. The emotional side is real, and it shapes how you act.

Some of this emotional experience is tied to financial stress. Bankrate reported that 43% of U.S. adults said money negatively impacts their mental health (Bankrate, 2024). That’s why if you are juggling multiple payments, you’ll likely feel stressed. Every additional debt account can add another worry to your day.

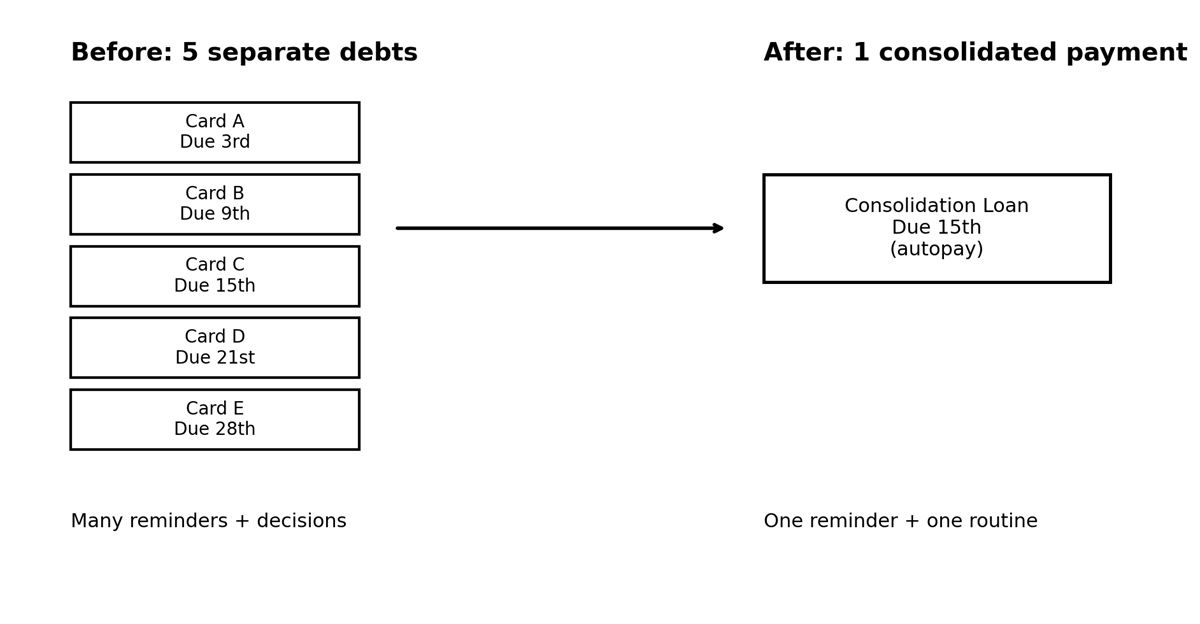

Example showing how 5 cards impact mental bandwidth

Five cards mean 5 due dates, 5 minimums, and 5 chances to forget. You’re also tracking which payments are set up for autopay and which you handle manually. One missed payment triggers fees and instantly raises stress.

|

Creditor |

Balance |

APR |

Due date |

Minimum |

|

Card A |

$2,100 |

24.99% |

3rd |

$65 |

|

Card B |

$3,450 |

19.99% |

9th |

$105 |

|

Card C |

$1,800 |

27.99% |

15th |

$55 |

|

Card D |

$4,600 |

22.49% |

21st |

$145 |

|

Card E |

$900 |

18.99% |

28th |

$35 |

When juggling multiple debts like in the example above, you feel like you’re always behind, even if you have a viable plan to manage it. Feeling stuck makes people less likely to check statements or plan. Additionally, under stress, the brain seeks quick comfort, leading to impulse spending or treats.

Why consolidation changes behavior, not just balances

Consolidation can lower your interest rate or monthly payments, which is helpful. But the real benefit is that having just 1 payment changes your habits. It gives you 1 clear goal instead of several small problems to manage. Seeing your progress each month can also keep you motivated.

Figure 1: multiple debts vs. one consolidated payment.

Zoom in: Member experience

A member who was not missing payments still felt exhausted from constantly moving money between accounts to avoid late fees. After consolidating into a single fixed payment, they described the biggest change as emotional: less checking, fewer mini-panics, and a routine they could keep, even during a busy month. With that breathing room, they stuck to a weekly spending limit and started building a small emergency cushion. They stopped viewing every email alert as a crisis and started enjoying managing their personal finances.

Consolidation works best when paired with habits that prevent balances from returning. In other words, debt consolidation psychology is about designing a payoff system you follow.

Math vs. Momentum — what actually helps people pay off debt

If you’ve ever tried to find the perfect way out of debt, you know that the best plan on paper doesn’t always work in real life. Often, the plan that works best is the one you can keep up with, even when life gets busy or stressful. That momentum is a mental boost that keeps you going.

Scenario comparison:

Option A: Saves you $20 per month in interest but requires 4 separate payments and constant tracking.

Option B: Turns the payoff into 1 automated payment with a clear end date.

Option B is more likely to help you avoid missed payments and late fees because it requires only 1 payment. If you have a busy schedule or struggle with decision fatigue, this simple approach works better than complicated systems you can’t keep up with.

It may not be for everyone, but if you know you burn out on repetitive administrative tasks, a plan that reduces cognitive load (fewer logins, fewer dates, fewer minimums) may be the right one for you. Seeing your single balance drop each month strengthens your “I can do this” mentality. That is why debt consolidation psychology values simplicity as much as savings.

Your credit union can help by offering structured consolidation options and transparent terms, plus support that is tailored to your situation. The goal is to align your monthly payment with your payday and your financial habits. You can also meet with a financial coach who can help you create a personalized debt payoff plan and provide guidance every step of the way.

If you want more step-by-step help, you can learn more about debt consolidation and other ways to manage debt. If stress is an issue, we also offer resources on financial stress.

When consolidation makes sense—and when it doesn’t

The final question is whether consolidation fits your situation right now. Consolidation is not a cure-all, and it is not always the first step. But when it reduces complexity and lowers cost, it is a smart move. The key is to evaluate both the numbers and the behavior you will need to succeed.

Characteristics of a good consolidation candidate include:

- Steady, reliable income: Consolidation works best when you can confidently make 1 fixed payment every month without relying on hope or overtime that comes and goes.

- Predictable monthly cash flow: If your bills and take-home pay don’t swing wildly, it’s easier to commit to a consistent payment schedule and avoid falling behind.

- Multiple high-interest debts: People carrying several credit cards (or other high-APR balances) benefit because consolidation simplifies payments and reduces the overall interest drag.

- A clear rate improvement opportunity: The numbers should make sense. Your consolidation rate, plus any fees, should be meaningfully lower than what you’re currently paying.

- Consistent payment history: Turn your payment discipline into faster progress by reducing friction and complexity.

- Enough creditworthiness to qualify for decent terms: You don’t need perfect credit, but you typically need some approval strength to get a rate that’s better than your current card APRs.

- Willingness to stop adding new debt: Consolidation only works long-term if you don’t refill the cards you just paid off. Otherwise, you can end up with both a consolidation loan and new credit card balances.

- A plan to automate and stay consistent: Candidates who set up autopay and align the due date with payday are more likely to follow through. Let the system carry you when motivation dips.

Situations where consolidation may not help

Consolidation may not make sense if your income is temporarily unstable or if the new loan has higher total costs. Also, it might not work out when you are trying to solve a spending problem without changing your habits. Be cautious if you are moving unsecured debt into a secured loan without a clear plan and full understanding of the risks.

Pair consolidation with a budget plan

If you consolidate debt but keep cards active without guardrails, temptation stays high. Consider lowering limits, moving cards out of reach, and following a budgeting plan that keeps your expenses in check.

Credit unions support long-term progress

If you are ready for consolidation, your credit union offers transparent pricing and personalized solutions that fit your situation. You likely want more than a loan and are looking for clarity, education, and a plan that fits your life. We also emphasize member education and support. Pairing consolidation with coaching and tools turns a short-term fix into a long-term habit change.

FAQs

Why does debt feel stressful even when I can afford the payments?

Because debt isn’t just a payment, it’s ongoing mental tracking. Multiple balances, due dates, and statements create constant reminders and decision fatigue. That extra cognitive load can increase anxiety and make follow-through harder, even when your budget technically works.

Does debt consolidation really help people pay off debt faster?

Yes. Consolidation may lower your interest rate, reduce late fees, and simplify payments. The biggest payoff advantage comes from consistency. With 1 payment that is easier to manage, you are less likely to miss payments or quit your debt repayment plan.

Is consolidation more about psychology than interest rates?

For many borrowers, yes. Interest rates matter, but staying consistent matters just as much. If simplifying your system reduces avoidance and improves habits, the psychological benefit can be the difference maker.

What types of debt can be consolidated?

Commonly, unsecured debts such as credit card debt and some personal loans can be consolidated. Some people also consolidate other debts with home equity products, but this introduces additional risk because your home may serve as collateral.

How can a credit union help with debt consolidation?

Your credit union can help you evaluate whether consolidation fits your situation by clearly explaining the options available to you. We can also offer structured products with transparent terms, plus education and tools, such as a debt payoff calculator, so that you can build a payoff plan that works for you. In some cases, your credit union may also partner with trusted non-profit organizations to provide additional debt solutions, counseling, or resources designed to support long-term financial stability.

Citations

Ong, Q., Theseira, W., & Ng, I. Y. H. (2019). Reducing debt improves psychological functioning and changes decision-making in the laboratory. Proceedings of the National Academy of Sciences, 116(15), 7244–7249. https://pmc.ncbi.nlm.nih.gov/articles/PMC6462060/

Bankrate. (April 30, 2025). Survey: 43% of Americans say money is negatively impacting their mental health. https://www.bankrate.com/banking/money-and-mental-health-survey/

*PLEASE NOTE: This article is intended to be used for informational purposes and should not be considered financial advice. Consult a financial advisor, accountant or other financial professional to learn more about what strategies are appropriate for your situation.

Related Resources

View All

10 min read

Smart Habits for Building Generational Wealth Over Time

Generational wealth doesn’t start on an equal playing field. Some inherit opportunities, while others inherit barriers that can be shaped by discrimination and trauma. No matter where you start, though, wealth-building is still possible by learning from the past and taking steps that help the next generation carry less weight. This article breaks down practical, realistic generational wealth strategies. These tips will work whether you’re starting from scratch or rebuilding after setbacks. As you read, keep one idea in mind: wealth is less about what you earn and more about what you keep, protect, and pass on.

10 min read

The Local Advantage: Why Local Credit Unions Continue to Win in 2026 and Beyond

Banking in 2026 is shaped by 2 expectations: strong digital access and real support. Those expectations aren’t going away anytime soon. That mix is why banking with a local credit union is desirable for everyday consumers.

10 min read

Love & Money: Having Honest and Productive Money Talks with Your Partner

Money can turn a normal moment tense, for instance, a late bill or surprise purchase can feel personal. In such situations, talking about money with your partner works best when it’s calm, planned, and respectful. With repetition, financial conversations in relationships feel more like teamwork and less like conflict.

10 min read

Credit Union vs. Bank: What “Member-Owned” Really Means

Most of us don’t choose a financial institution because we love paperwork. We choose one because we want paychecks to land on time, cards to swipe reliably, and loans to feel fair when a big life expense shows up. One phrase you’ll hear most when comparing banking options is member-owned credit union. If you’ve ever wondered what is a credit union or compared a credit union to a bank, you’re in the right place to learn more.

10 min read

Fell Out of Love With Your New Year’s Resolutions? Reset Your Finances and Rebuild Momentum

If your 2026 resolutions started strong and then fizzled, you’re not the only one. That doesn’t cancel your New Year money goals; it likely just means you need a simpler plan. Use this guide for a February-friendly financial reset that keeps you moving without guilt.

10 min read

Maximizing Your Credit Union Membership Beyond Checking

Opening a checking account is usually the first introduction to your credit union. But credit union membership can do more than process transactions. It can help you plan, automate, and make decisions with fewer surprises. Below, you’ll see 4 areas where membership offers support beyond checking.

10 min read

Setting Meaningful Money Resolutions with Your Kids

Kids don’t need complicated tools to learn about money. What’s more important is that they see how money is used in the world around them through experience and the development of good habits. To create effective money resolutions with your kids, you first need to develop a routine they can follow. When you set goals together, you’re also building trust and shared language around choices.

10 min read

5 Steps to Recover from Increased Holiday Spending

The holidays can be joyful and expensive at the same time. One more gift here, an extra dinner there, a quick trip you didn’t plan for, and then the new year arrives, and the statements feel louder than the celebrations did. If you’re dealing with the aftermath of increased holiday spending, you’re not alone. Here are 5 practical steps to help your holiday spending recovery. The point isn’t to feel guilty or to fix everything overnight. It’s about getting clear on your numbers and making a realistic plan for your post-holiday debt. Then, build a few guardrails so next year is easier.

10 min read

How Your Credit Union Deposits Strengthen Local Communities

A deposit at a credit union is a simple transaction. But behind the scenes, it has a domino effect on local communities. That same deposit can help a neighbor buy a car, a family move into a first home, or a small business add another job, creating significant community impact. Plus, your money stays closer to the people and places you care about.

If you bank with a credit union, you’re part of a member-owned system built to serve members first. That difference shows up in real ways, from lending decisions to education programs and local giving.

10 min read

Why Debt Consolidation Is About Psychology, Not Just Numbers

Have you ever looked at your budget and wondered how you will cover all your bills? If you’re feeling constantly behind as you navigate your debt, there is a reason. Debt is math, but it also requires attention and introduces stress and mandatory routines. Each extra account adds another due date and another minimum payment. Even worse, it leaves you feeling like you are one mistake away from chaos.

In debt consolidation psychology, the numbers matter, but so does the structure of your debt system. When the plan is easier to run, you follow through more often. That follow-through is what pays off debt.

12 min read

Financial Planning in 2026: A Fresh Start Guide

If money felt harder to come by in 2025, you’re not alone. In the West Region, which includes Colorado, consumer prices were up 3% for the 12 months ending in November 2025 (U.S. Bureau of Labor Statistics, 2025). Mortgage rates also stayed elevated, with the average 30-year fixed rate ending 2025 at 6.15% (Freddie Mac, 2025). And in Colorado, housing remained a major pressure point. Rocket Homes estimated that the average monthly mortgage payment rose from $1,836 in 2024 to $1,900 in 2025 (Steinberg, 2025).

While New Year's motivation is powerful, it fades fast, and the current financial landscape demands a lasting plan. Even if inflation has cooled from peak levels, prices and borrowing costs will shape your everyday decisions. That’s why the small choices you make in financial planning 2026 will have an outsized impact.

Our simple financial planning guide sets the stage for repeatable, sustainable actions. You don’t need a perfect spreadsheet to start. You need a few repeatable decisions: set targets, build a workable budget, protect yourself with an emergency savings buffer, and schedule quick check-ins

10 min read

Winning Financial Moves: How to Create a Budget & Maximize Every Dollar

A budget is simply a written plan for your money, yet only 42% of Americans keep one consistently (NFCC, 2024). When you chart where every dollar goes, three things happen: you gain clarity, you control spending before it occurs, and you feel more confident about emergencies. In short, a budget is a way to make sure you can cover your expenses from month to month — a calm antidote to paycheck panic. It creates financial stability and supports your financial goals; read on to learn how to create a budgeting plan.