5 min read

Exploring the Advantages of Digital Banking: Features, Security, and Tips

-

-

Copied link to Clipboard!

Copied link to Clipboard!

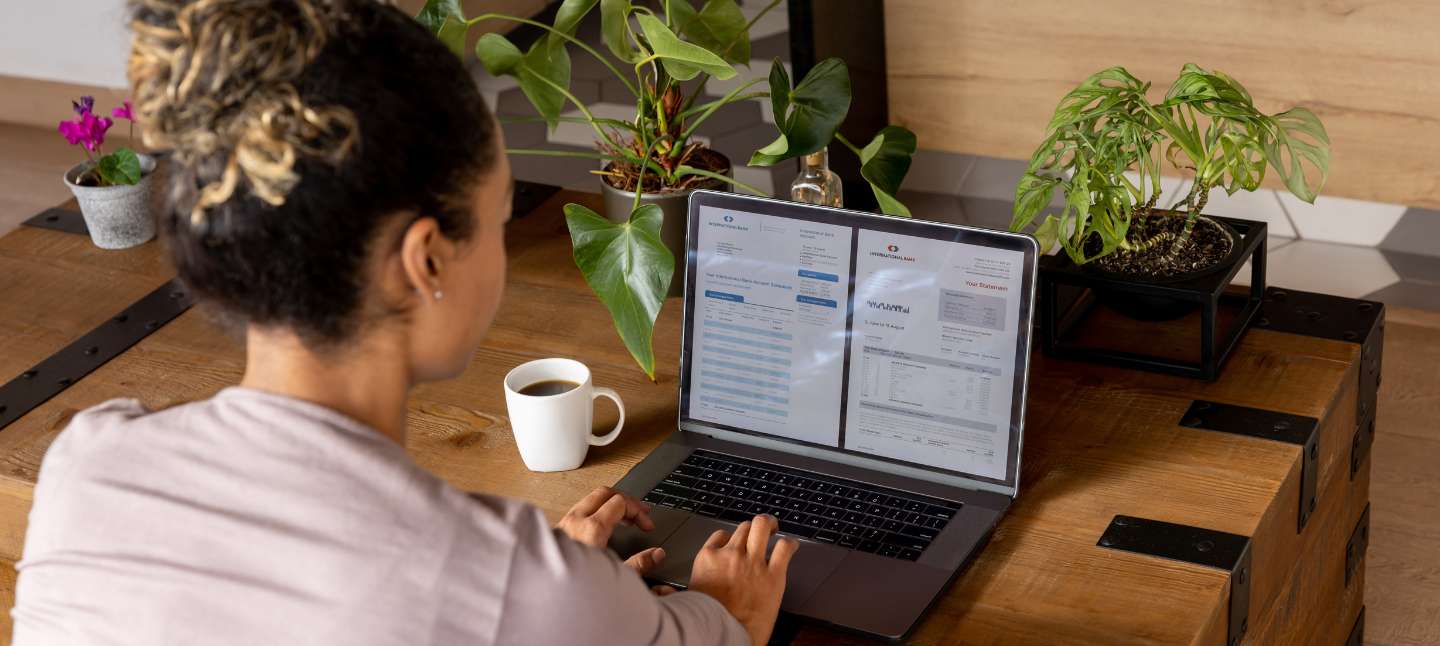

Digital banking lets you securely manage your money on the go. You can access nearly all the same benefits and features on your mobile device or computer without visiting a brick-and-mortar branch. Digital banking apps also use security features such as two-factor authentication and facial recognition.

You have many options for where and how you manage your money. Thanks to digital banking, you no longer need to go to a physical bank or credit union to open an account, make a deposit, or transfer money between accounts. You can manage your money digitally using your smartphone, tablet, or computer and save time from commuting to your local financial institution. Convenient digital banking is widespread, and your current bank or credit union probably already offers this service.

What is digital banking, and how does it compare to visiting a branch in person? Explore the benefits of digital banking and use these tips to help keep your money safe.

LESSON CONTENTS

What is digital banking?

Digital banking means managing your money using an electronic or digital platform, such as a website or mobile banking app. You can access a financial institution’s products and services by logging into the app or website on a smartphone, tablet, or computer without visiting a local service center in person.

Both online banking and mobile banking fall under the umbrella of digital banking. Online banking refers to banking services provided over the internet, such as a website. While mobile banking means accessing these services on a mobile device like a tablet or smartphone. Downloading a digital banking app from your financial institute to your mobile device should be free.

To bank digitally, you must log in to your account via the app or website using a secure username and password. If you have an account but don’t have digital banking yet, you should be able to set it up online in just a few minutes or download your financial institution’s app from an official app store. If you don’t already have a checking or savings account, many financial institutions let you open a new account on their website. Or you can visit a local branch in person to get started. Then you’ll be ready to set up digital banking.

With digital banking, once you log in, you can check your account balance, transfer money between your accounts or to another financial institution, and deposit checks by uploading a photo of the front and back of the check. If you have a loan, you can check your remaining balance, track interest, and make payments in just a few easy clicks.

Nearly all financial institutions offer digital banking in addition to in-person banking. However, some banks exist entirely online, so you must manage all your accounts digitally via their app or website.

What are the benefits of digital banking?

Digital banking is revolutionizing the way people manage their finances. It is the fastest way to access your account. That way you can spend more time making informed financial decisions and less time driving to your financial institution to manage your account. You’ll also be in good company. It has been reported that almost 80% of Americans prefer to bank digitally.

Managing your money digitally instead of in person can unlock many benefits and banking features without visiting your local branch. This technology is designed to make life easier by offering:

Anywhere, anytime banking

Digital banking gives you the freedom to access financial products and services 24/7. With internet access or a mobile device, you can conveniently log in to your account and manage your money hassle-free. You don’t have to worry about visiting your local financial institution during their hours. Instead, you can bank nights, weekends, and even holidays. You can see your accounts in one location to get an overall view of your current finances. Some apps and websites also offer built-in budgeting and planning tools that help you keep track of important goals and trends. For example, they can track how much you spend vs. how much you earn every month to encourage you to save. And some even let you see your accounts across different financial institutions for a comprehensive view of your entire financial health.

Personal help when you need it most

If you have a question about your account or need help with your finances, you can often get the answer right away on your mobile device or computer. Most credit unions and banks offer digital help, such as instant chat and over-the-phone support. The chat feature is usually available 24/7, so you can quickly get the answers you need.

Strong security

Digital banking apps and websites are designed to be secure. Security is a priority within the financial industry and that includes following (and in some cases exceeding) current industry digital security standards. A typical security feature includes sending a notification of suspicious activity on your account. You can also take steps to support your security. For example, when you create a digital banking e-account, you will choose your password and username. Experts recommend creating a strong password by using a unique phrase or list of characters that you can easily remember. Also, choose multi-factor authentication for an additional layer of security if it’s offered, but not mandatory, at your financial institution. Some financials will also send you a notification via text or email with a secure code to verify your identity. Important: Do not share this code with anyone.

Additionally, some apps and websites also let you log in using facial recognition or your fingerprint.

Automated services to save time

Paying your bills and getting paid is much easier when you use electronic bill pay within digital banking. Bill pay lets you both receive and pay bills electronically. It can be used for one-time payments or recurring bills, like rent, loans, utilities, and credit card bills. Payments can also be automated by selecting which account you’d like the payment to be deducted from. That way, you don’t have to worry about forgetting or falling behind on your bills.

The same is true of direct deposits. You can have your paycheck, Social Security payment and other regular checks automatically deposited into your account as soon as they’re available. You won’t have to worry about losing checks or having someone trying to cash them.

Also, many digital banking apps and websites are compatible with digital payment apps like Venmo, PayPal, and Apple Pay.

Fraud protection on the go

Fraud prevention should always be top of mind. If someone steals your debit or credit card, you can quickly and easily log in to your account and freeze the card to prevent anyone from using it. Or if you misplace your card, you can freeze its use (just in case) and then unfreeze it once you find it. You can also sign up to receive notifications for every transaction.

*PLEASE NOTE: This article is intended to be used for informational purposes and should not be considered financial advice. Consult a financial advisor, accountant or other financial professional to learn more about what strategies are appropriate for your situation.

Related Resources

View All

10 min read

Smart Habits for Building Generational Wealth Over Time

Generational wealth doesn’t start on an equal playing field. Some inherit opportunities, while others inherit barriers that can be shaped by discrimination and trauma. No matter where you start, though, wealth-building is still possible by learning from the past and taking steps that help the next generation carry less weight. This article breaks down practical, realistic generational wealth strategies. These tips will work whether you’re starting from scratch or rebuilding after setbacks. As you read, keep one idea in mind: wealth is less about what you earn and more about what you keep, protect, and pass on.

10 min read

The Local Advantage: Why Local Credit Unions Continue to Win in 2026 and Beyond

Banking in 2026 is shaped by 2 expectations: strong digital access and real support. Those expectations aren’t going away anytime soon. That mix is why banking with a local credit union is desirable for everyday consumers.

10 min read

Love & Money: Having Honest and Productive Money Talks with Your Partner

Money can turn a normal moment tense, for instance, a late bill or surprise purchase can feel personal. In such situations, talking about money with your partner works best when it’s calm, planned, and respectful. With repetition, financial conversations in relationships feel more like teamwork and less like conflict.

10 min read

Credit Union vs. Bank: What “Member-Owned” Really Means

Most of us don’t choose a financial institution because we love paperwork. We choose one because we want paychecks to land on time, cards to swipe reliably, and loans to feel fair when a big life expense shows up. One phrase you’ll hear most when comparing banking options is member-owned credit union. If you’ve ever wondered what is a credit union or compared a credit union to a bank, you’re in the right place to learn more.

10 min read

Fell Out of Love With Your New Year’s Resolutions? Reset Your Finances and Rebuild Momentum

If your 2026 resolutions started strong and then fizzled, you’re not the only one. That doesn’t cancel your New Year money goals; it likely just means you need a simpler plan. Use this guide for a February-friendly financial reset that keeps you moving without guilt.

10 min read

Maximizing Your Credit Union Membership Beyond Checking

Opening a checking account is usually the first introduction to your credit union. But credit union membership can do more than process transactions. It can help you plan, automate, and make decisions with fewer surprises. Below, you’ll see 4 areas where membership offers support beyond checking.

10 min read

Setting Meaningful Money Resolutions with Your Kids

Kids don’t need complicated tools to learn about money. What’s more important is that they see how money is used in the world around them through experience and the development of good habits. To create effective money resolutions with your kids, you first need to develop a routine they can follow. When you set goals together, you’re also building trust and shared language around choices.

10 min read

5 Steps to Recover from Increased Holiday Spending

The holidays can be joyful and expensive at the same time. One more gift here, an extra dinner there, a quick trip you didn’t plan for, and then the new year arrives, and the statements feel louder than the celebrations did. If you’re dealing with the aftermath of increased holiday spending, you’re not alone. Here are 5 practical steps to help your holiday spending recovery. The point isn’t to feel guilty or to fix everything overnight. It’s about getting clear on your numbers and making a realistic plan for your post-holiday debt. Then, build a few guardrails so next year is easier.

10 min read

How Your Credit Union Deposits Strengthen Local Communities

A deposit at a credit union is a simple transaction. But behind the scenes, it has a domino effect on local communities. That same deposit can help a neighbor buy a car, a family move into a first home, or a small business add another job, creating significant community impact. Plus, your money stays closer to the people and places you care about.

If you bank with a credit union, you’re part of a member-owned system built to serve members first. That difference shows up in real ways, from lending decisions to education programs and local giving.

10 min read

Why Debt Consolidation Is About Psychology, Not Just Numbers

Have you ever looked at your budget and wondered how you will cover all your bills? If you’re feeling constantly behind as you navigate your debt, there is a reason. Debt is math, but it also requires attention and introduces stress and mandatory routines. Each extra account adds another due date and another minimum payment. Even worse, it leaves you feeling like you are one mistake away from chaos.

In debt consolidation psychology, the numbers matter, but so does the structure of your debt system. When the plan is easier to run, you follow through more often. That follow-through is what pays off debt.

12 min read

Financial Planning in 2026: A Fresh Start Guide

If money felt harder to come by in 2025, you’re not alone. In the West Region, which includes Colorado, consumer prices were up 3% for the 12 months ending in November 2025 (U.S. Bureau of Labor Statistics, 2025). Mortgage rates also stayed elevated, with the average 30-year fixed rate ending 2025 at 6.15% (Freddie Mac, 2025). And in Colorado, housing remained a major pressure point. Rocket Homes estimated that the average monthly mortgage payment rose from $1,836 in 2024 to $1,900 in 2025 (Steinberg, 2025).

While New Year's motivation is powerful, it fades fast, and the current financial landscape demands a lasting plan. Even if inflation has cooled from peak levels, prices and borrowing costs will shape your everyday decisions. That’s why the small choices you make in financial planning 2026 will have an outsized impact.

Our simple financial planning guide sets the stage for repeatable, sustainable actions. You don’t need a perfect spreadsheet to start. You need a few repeatable decisions: set targets, build a workable budget, protect yourself with an emergency savings buffer, and schedule quick check-ins

10 min read

Winning Financial Moves: How to Create a Budget & Maximize Every Dollar

A budget is simply a written plan for your money, yet only 42% of Americans keep one consistently (NFCC, 2024). When you chart where every dollar goes, three things happen: you gain clarity, you control spending before it occurs, and you feel more confident about emergencies. In short, a budget is a way to make sure you can cover your expenses from month to month — a calm antidote to paycheck panic. It creates financial stability and supports your financial goals; read on to learn how to create a budgeting plan.