6 min read

What is a Loan Amortization Schedule?

-

-

Copied link to Clipboard!

Copied link to Clipboard!

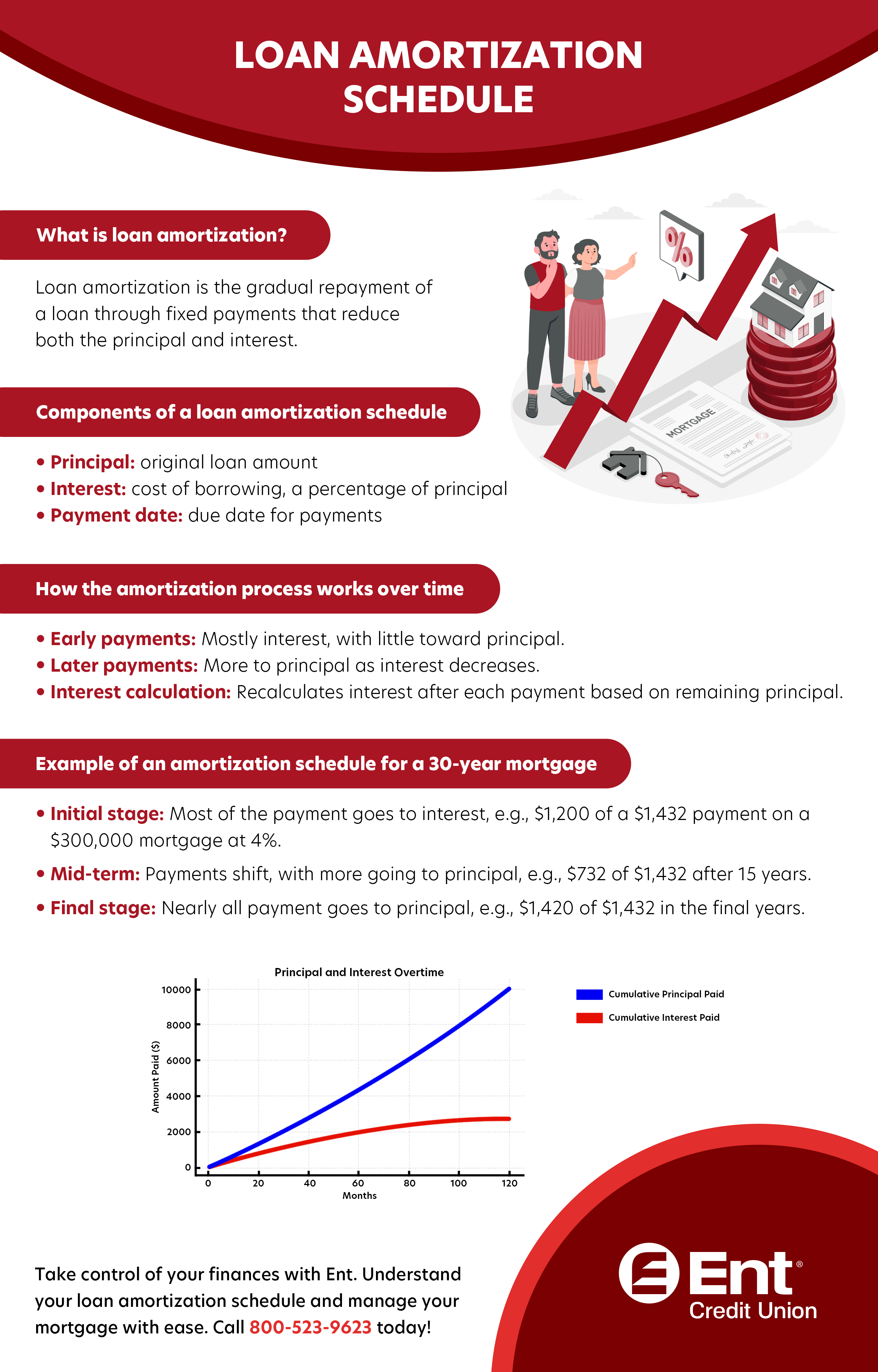

When you buy a home for the first time and take out a home loan, you will need to pay back the amount borrowed plus interest over a set period of time. The total amount of the loan, including the principal plus interest, is split into equal monthly payments. Every payment will go towards both the principal and interest. A loan amortization schedule shows you what percentage of your monthly payment goes towards the principal vs. interest. These percentages will change over time as you get closer to paying off the loan. Use a loan amortization schedule to determine how much you are paying in interest over the life of the loan.

Lesson Notes:

Lesson Notes:

- A loan amortization schedule shows what percentage of your monthly loan repayment is going towards interest vs. the principal amount.

- Most of your payments will go towards interest during the beginning of the loan, but nearly all your payments will go towards paying off the principal as the loan continues to amortize.

- You can use a loan amortization schedule to track how much equity you have based on how much you have put towards the principal.

LESSON CONTENTS

What does a loan amortization schedule show?

A loan amortization schedule is a chart of all the monthly payments you will need to make until you pay off the loan entirely. If you have a loan with a fixed home interest rate, such as a fixed-rate 30-year mortgage, your monthly payment will stay the same every month, but the percentage of money going towards interest will change as you pay down the principal.

When you begin making payments on the loan, a large percentage of your monthly payment will go towards paying off the interest that has accrued on the loan. As you pay down the principal amount over time, you will accrue less interest every month and year, which means more of your money will go towards the principal. By the time you are close to paying off the loan, a large portion of your monthly payment will go towards the principal, with a much lower percentage going towards interest.

The loan amortization schedule shows every payment you will make during the repayment period. Every payment then gets broken down into a set of percentages that represent how much is going towards the principal vs. interest. You can use this chart to see how your monthly payment is being allocated.

The length of the loan amortization schedule depends on the length of the repayment plan, which may last anywhere from several months to several decades, depending on the type of loan. Having a longer amortization period will lower your monthly payment, but you will generally pay more in interest over the life of the loan. Shortening the amortization period can increase your payment, but you will typically pay less in interest and get out of debt that much faster.

How to use a loan amortization schedule

The loan amortization schedule is helpful because it shows you how much you pay in interest in every month. You can use the chart to keep track of your progress in terms of paying off the principal amount and getting out of debt.

You can also use the chart to calculate how much equity you have in your home or vehicle. Calculate how much money you have put towards the principal since you started making payments on your loan. To calculate equity, determine the value of the home, divided by the remaining principal balance to see what percentage of you have in equity.

You are free to pay more than the required amount when repaying your loan every month. Depending on your long-term , you may want to consider putting more of your money towards your debt to reduce interest paid over time. Any extra money you put towards the loan will go entirely to the principal to help you pay off the loan as quickly as possible. The sooner you pay off the principal, the faster you will get out of debt. Keep in mind your original amortization schedule doesn’t account for additional payments to principal.

Some loan types only require you to pay the interest that has accrued on your loan during a draw period. In this case, 100% of your monthly payment will go towards interest. Consider paying more than the required amount to start paying down the principal before the repayment period begins.

Use a loan amortization schedule to see what percentage of your monthly payments will go towards interest based on your current repayment plan.

*PLEASE NOTE: This article is intended to be used for informational purposes and should not be considered financial advice. Consult a financial advisor, accountant or other financial professional to learn more about what strategies are appropriate for your situation.

Related Resources

View All

10 min read

How Do I Refinance My Mortgage and Consolidate Debt?

Paying different credit card bills, a personal loan, and a 30-year mortgage every month can feel like managing a dozen spinning plates at once. Refinancing your home loan to combine higher-rate balances into a single, lower-rate mortgage — known as a debt consolidation refinance — transforms that juggling act into one predictable payment.

How do you refinance your mortgage for debt consolidation? We break down how a mortgage debt consolidation refinance works, when the math favors you, and how to weigh the risks and rewards.

12 min read

What are the Differences: VA Loan vs Conventional Loan

Choosing the right credit union mortgage loan shouldn’t feel like decoding a secret manual. Yet when people first compare a VA loan vs a conventional loan, the jargon — funding fees, PMI, conforming limits — can stall the search before it starts. This guide strips away the haze by lining up the two products feature by feature. You will see how each loan handles down payments, credit scores, interest rates, and closing costs, and you’ll finish with a checklist that points you toward the option most likely to fit your budget, service record, and future plans.

5 min read

Why Are Mortgage Rates So High?

If you are mortgage shopping this year, you are feeling the rate sticker shock. The average 30-year fixed rate sits around 7 percent, more than double the record lows of 2021 (Mortgage News Daily, 2025). Why are mortgage rates so high today? In short, mortgage rates are higher because the bond market — where mortgage prices are set — adjusted the cost of money. This shift came after the Federal Reserve responded to a period of high inflation. A careful look at policy, prices, and growth helps explain the surge in rates and the impact of mortgage rates on housing in 2025 and beyond.

10 min read

Can You Purchase a Car with a Credit Card?

Ask any efficiency-minded car shopper, and the first question is usually: Can you buy a car with a credit card? In theory, the answer is yes — you absolutely can. In practice, the path is littered with card-issuer rules, dealer surcharges, and interest-rate landmines that can turn a clever rewards strategy into an expensive misstep. New-vehicle prices hit an average of $48,699 in April 2025, a 2.5% month-over-month increase (Cox Automotive, 2025). At the same time, Woolsey (2025) notes the median credit card APR climbed to 24.2% in March 2025. That combination of sticker shock and swipe costs makes it vital to understand every angle before you hand the finance manager a piece of plastic.

10 min read

A Comprehensive Guide to Credit Union Home Loans in Colorado

Buying a home is one of the most significant financial decisions you'll make in your lifetime. If you're considering purchasing a home in Colorado, one of the best options is to obtain a home loan through a credit union. Why is choosing a credit union for your home loan advantageous? Learn more below, including the types of home loans in Colorado available at credit unions, how to qualify, and the step-by-step process to get you into your dream home.

10 min read

How to Qualify for a Home Equity Line of Credit (HELOC)

Home values continue to soar, and U.S. households have accumulated over $35 trillion in home equity (St. Louis Fed, 2024). If you are among those who have done so, you can borrow against this financial resource for various needs, such as home improvements, education expenses, or consolidating high-interest debt. Below, we outline how to qualify for a Home Equity Line of Credit (HELOC) to prepare you for this opportunity.

12 min read

A Guide to the Different Types of Home Loans in Colorado

Purchasing a home is a dream for many. In this process, understanding the types of home loans in Colorado sets you on the right track to get a mortgage that suits you. Therefore, let's explore the various types of mortgage loans in Colorado and their benefits and eligibility requirements. You will also learn how Ent Credit Union can assist you in home-buying.

12 min read

Best Practices for Using a Home Loan Calculator in Colorado to Get Accurate Results

One of the most consequential financial decisions you will make in your lifetime is purchasing your home. In Colorado's unique housing market, using a home loan calculator in Colorado can provide invaluable insights. Read on for effective best practices in using these calculators to get accurate results.

12 min read

Taking On Your First Home Mortgage? Here's Our First-Time Homebuyer’s Guide to Home Loans

The journey to homeownership is exciting, especially for first-time buyers. However, the complexities of mortgages, understanding rates, and knowing what steps to take can sometimes become overwhelming. This guide demystifies the process of securing your first home mortgage.

8 min read

Buying a Car for the First Time

Starting your financial journey is like setting off on an exciting road trip. You’re gearing up for major life events, like buying a car for the first time. In planning for this event, remember that you are making decisions that should benefit you in the long run. Therefore, it’s important to understand the processes and the appropriate financial products to achieve your goal. This guide shows the critical steps of purchasing your first car.

7 min read

Choose the Right Mortgage Refinance Plan

Is refinancing the right move for me? It depends. Refinancing your mortgage loan can be a strategic financial move, saving you money on interest, lowering your monthly payments or shortening your term.

12 min read

Documents for Refinancing a Mortgage: A Comprehensive Guide

Refinancing a mortgage offers a pathway to adjust your financial burdens by changing the terms of your home loan in Colorado. There are several reasons for refinancing (Freddie Mac, 2024), including lowering your interest rate, reducing your monthly payment or changing the mortgage term. Other common reasons include switching from an adjustable rate to a fixed rate or tapping into your home equity. However, the process involves gathering and submitting several refinance documents. Here’s a guide to help you understand what you'll need to provide to refinance your mortgage.